For those Chief Financial Officers who may have recently joined a nonprofit organization, you are likely wondering how to choose a 403b plan. As you review the current retirement plan, what are the important facts to know?

Contact your Plan Administrator and your Investment Advisor so you can be briefed on the plan. Documents you should have on file for your review are:

- Summary Plan Description and Plan Document

- From your administrator’s portal, you should be able to surmise size of plan, number of active participants, employer match contribution year-to-date, number of loans outstanding

- Form 5500 or 5500-SF filing for the most recent fiscal year

- A copy of the plan audit if your organization has over 100 employees (note the 80-120 Participant Rule)

- Retirement Plan Investment Policy

- Confirmation of the Fidelity Bond

- List of investment funds in the plan

- Documents and information relating to participant education

Unfortunately, we often find the retirement plan documentation is lost or partially complete when a new CFO, Director of Finance, Human Resources Manager or Executive Director comes on board. Yet, it is a good time to take stock of the benefits and potential liabilities that exist with the current retirement plan.

Unfortunately, we often find the retirement plan documentation is lost or partially complete when a new CFO, Director of Finance, Human Resources Manager or Executive Director comes on board. Yet, it is a good time to take stock of the benefits and potential liabilities that exist with the current retirement plan.

Here are a few areas to review:

1. Recordkeeping and Administration

Are you receiving the service and accessibility you need for the plan? We had one client whose previous Administrator could not properly set-up Plan Sponsor access for the new Human Resources manager. In addition, she was unable to obtain accurate reports or confirm how much they were paying in fees. It seems like a simple, easily fulfilled request, right?

However, the past 10 years has seen many acquisitions, mergers and changes in the Retirement Plan Administration business as large companies sell off portions of their retirement businesses (e.g., Empower acquired Mass Mutual’s Retirement Plan Business in 2020; Wells Fargo sold its Retirement Plan & Trust business to Principal Group in 2019; and PCS Retirement acquired Aspire Financial Services in 2019). Smaller companies and nonprofits (less than 100) are often lost in the shuffle during these changes and therefore the continuity with the Administrator and Recordkeeper is lost.

Is the platform easily accessible by employees? During the pandemic, it was especially important that retirement plan participants have easy, online access to their retirement plan. What are the recordkeeping and administration fees and how to they compare with the current marketplace?

2. Participant Education

Given current economic conditions, many employers are finding the need for their employees to receive additional financial education. Has your current Plan Investment Advisor or Plan Administrator met the educational needs of your employees? At Fairlight, we often work with plans with under 100 employees. Therefore, we can offer a more customized training approach and service to employees. This includes annual one-to-one financial planning discussions with employees.

What type of digital, educational content does the Plan Advisor and/or Plan Administrator provide? Are there videos, blogs, research information on the investments available?

3. Investments

Review the investment line-up with your Plan’s Investment Advisor. Are there too many investment choices for participants? Are there target date fund options for participants? Does the plan offer a Qualified Default Investment Alternative (QDIA)? This option in a plan defaults a participant into a target date or balanced fund in the absence of a participant directive. In other words, if the employee sets up a contribution but forgets to choose an investment option, he or she will be defaulted into QDIA.

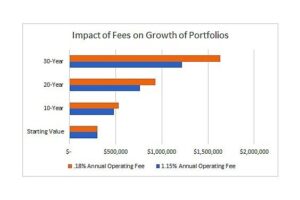

What are the investment fees in the plan? Are they reasonable? See the chart below, “Impact of Fees on Growth of Portfolios”, as an example of how investment fees inside the Retirement Plan can impact participants’ overall returns. Our video here explains more about fees.

Have your employees asked about social impact or socially responsible investment choices in your retirement plan? For nonprofit organizations, it’s becoming increasingly important to select choices which reflect their mission and impact. There are now more socially responsible or ESG investment options for Retirement Plans.

your retirement plan? For nonprofit organizations, it’s becoming increasingly important to select choices which reflect their mission and impact. There are now more socially responsible or ESG investment options for Retirement Plans.

The devil is in the details when you peek under the hood of your plan.

You can and should contact your Plan Advisor and your Plan Administrator for assistance in this process. At Fairlight, we are also here to help if you have questions or want to seek a second opinion on your plan.

Related Articles:

403 B Distributions Rules are Becoming a Hot Topic – What Should Employees and Employers Know?

Savings, Investing & 403 B Advice Rarely Changes – So Why Do We Forget it?

Related Videos:

Talk to the financial experts at Fairlight Advisors to learn more about managing your nonprofit’s investments. Schedule a free consultation today!

Fairlight Advisors

Latest posts by Fairlight Advisors (see all)

- Market & Economic Snapshot Q1 2026 - April 29, 2026