The need for affordable housing in the Bay Area was a crisis before the onslaught of the COVID pandemic and the resulting economic recession. The situation become more dire as time goes on, particularly since talks in Congress still are stalled on a new economic relief package. The Social Impact Advisory Group asked experts in the area of housing—nonprofit leaders, real estate developers and investors—about the affordable housing ecosystem and how they are collaborating and innovating to address this crisis. This is a summary of our discussion.

The Source of the Housing Crisis in the Bay Area

KATE COMFORT HARR, Executive Director of HIP Housing Okay, so how did we get here? This is a focus particularly on San Mateo County. We’re in a county that’s bordered on both sides by water; we’ve got the bay and we got the ocean on either side of us. We’ve got San Francisco County to the north Santa Clara County to the south. And in between, in San Mateo County, about 70% of our land is protected land. And that’s something that we all cherish and really don’t want to change. So that means that the portion of buildable land is a very fine strip that runs primarily along the bay side with a little bit on the coast. With so much restriction in how and where you can build, what ends up happening is the cost of land is driven way, way up. On top of that, you’ve got construction costs that are driven up, which ultimately lead to higher rents. Once housing is built—that’s if you can get it built at all—is there really are no market forces in San Mateo County that allow for affordable housing. We have an abundance of high paying jobs and people who can pay high rents. And as a result, those who can’t pay those rents are pretty much forced out. We’ll never be able to build enough to cover the gap of what we have in terms of people who need housing and people who have access to housing.

HIP Housing

Between 2010 and 2017, we added 84,000 new jobs to San Mateo County, but only 7,000 units of housing. That’s a twelve-to-one ratio. It’s not sustainable. And people don’t realize that for every one high tech, high paying job, you create seven service positions. So not everybody who’s coming into the workforce is going to be high paid.

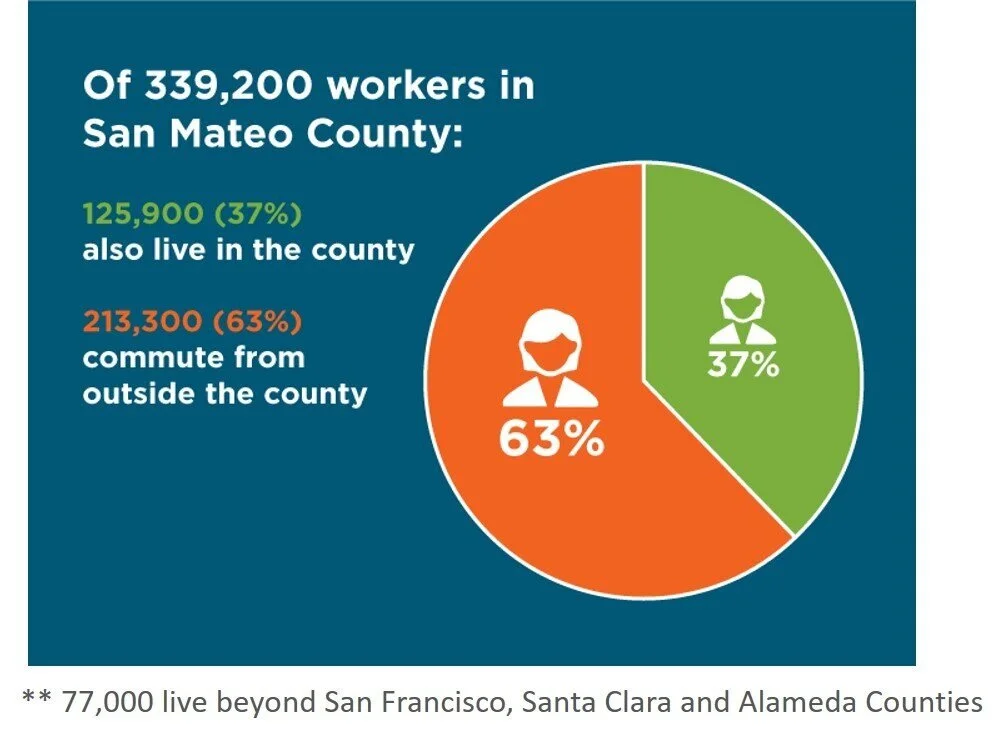

So what does our workforce look like? We have about 340,000 jobs in our county. Of those 213,000 plus are commuting from outside of San Mateo county. That means they have to come in and out and in and out every single day. 77,000 of those who are commuting are coming from beyond San Francisco, Santa Clara and Alameda County’s. So what does that mean? Traffic. People assume that if you bring more housing, you’re going to bring more traffic. But imagine if 212,000 people didn’t have to commute in and out if they lived close to their jobs? If they could walk or bike or take transit? That actually reduces the intensity of the traffic.

Another point to remember is, it’s really the lower paid workforce who’s forced out. People who can pay higher rents will likely stay as best they can. But it’s those lower paid workers, the service workers, the folks who make this such a great community to live in, that are forced out. We also have some of the highest transportation costs in the country between insurance, gas tolls for bridges, the people who can least afford it are being pushed out. So eventually they get to the point where they can’t afford to live here, but they can’t afford to commute either. And that puts us in a real risky position for having the services available that we need: school teachers, baristas, all the kinds of things that the whole range of a workforce who aren’t necessarily high-tech/high-paid. So that’s a little bit of how we got here; we have confined buildable space, we have an abundance of great jobs, we actually also have an abundance of lower paid workforce, and no true market forces that will ever allow us to create affordable housing naturally. So we have to be intentional about it. We have to think about it and find ways to bring more affordable housing and preserve that.

How Real Estate Developers Evaluate a Housing Project

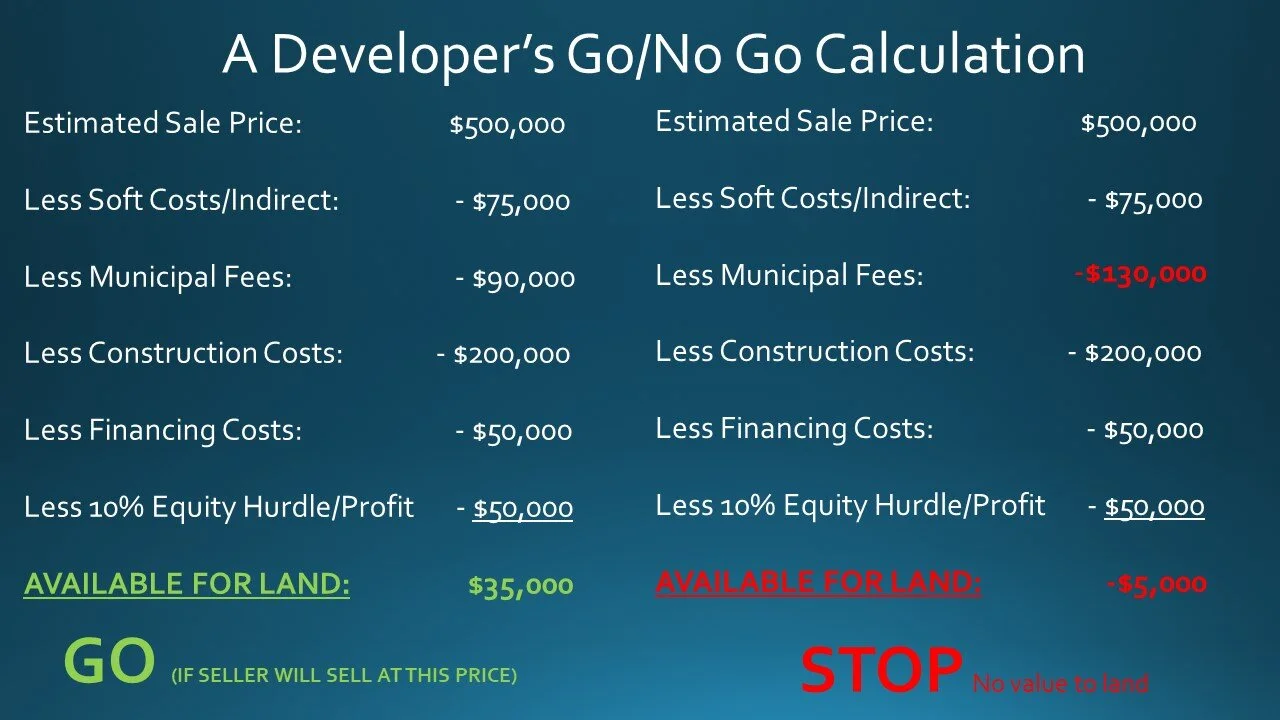

JONATHAN FEARN, SR. DIRECTOR, DEVELOPMENT at GREYSTAR It’s really kind of binary; can you sell something for more than it costs to build it, in essence. So at the risk of oversimplifying things, you start with what you think your final revenue is going to be and you take out all of your costs. What you have at the end is a thing called a land residual, which is what you are able to give a land owner to purchase their land. Now that obviously has to be at a level that the landowner will accept. But many, many, many things can impact whether or not a developer will move forward with a project. I have highlighted this because, if your fees go up per unit, the project then ceases; you no longer have the ability to provide any kind of payment for the land. But that could be anything. Developers work on spreads. They don’t work on total dollar amounts and that’s important because number one, if a developer meets its hurdle, we will proceed on a project regardless of the cost, or the top line revenue.

The second thing is that land is very, very valuable and very, very sought after. So when we talk about cost savings in a project, if our construction costs were to go down per unit, that would most likely end up in the hands of the land owner because we would then have more money to provide for the landowner, which would make us more competitive.

Greystar

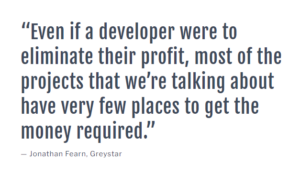

The other thing I’ll just say is that people say, “Well, why can’t you guys just take less profit?” And it’s an interesting question. Even if a developer were to eliminate their profit, most of the projects that we’re talking about that are being constructed in San Mateo County, or high density apartment complexes class, developers have very few places to get the money required, either from the equity side or the debt side. Those institutional capital sources do not have to go into real estate. That money flows where they can get the best return for their money, and so if they can get money in stocks or some other alternative investment, they will do so. So developers really don’t have many options when it comes to the returns that are required for the projects that we’re talking about.

Ways to Drive Down the Cost of Housing

RAJ PATEL, INVESTOR, GOLDEN GATE INCLUSION FUND I’ve always been passionate about innovation and I love the idea of solving the housing crisis in San Francisco, because it touches all of us in the broader nine county Bay Area, including San Mateo County. Up until recently, there’s been a generalized focus on affordable housing and today we’re seeing more expansion into the concept of workforce housing, which catches a whole group of potential or current residents of San Francisco and the broader nine county Bay Area that may not fit the technical definition of income brackets to qualify for affordable housing, yet also are key contributors to the economy. Workforce housing is for a group of people who may not fit within the within the affordable housing definition but also, based off of their own income, simply cannot afford market rate. The exciting part of real estate development, and this is a little bit based off of what Jonathan mentioned, is how do we address the cost side of construction? And so what we’re focused on is how do we really innovate interior design, such that we are able to reduce the actual price per square foot, and also also access some of the more innovative construction approaches. It is possible to innovate even in construction materials and go beyond traditional material configurations of steel, concrete, wood, and focus on almost pure steel construction, but instead of just applying that to single family, we might consider that for high density urban, multi-story urban residential. So I think when we look at the configuration, the macroeconomic issues with constructing housing in the grid in the Bay Area, we need to not obsess so much on what what labor costs might be, for example, which is essentially built into the cost side, but really push the envelope on how to innovate further reduced on the cost side outside of labor.

San Mateo County is really interesting because I think, as was already mentioned, when you look at the map, we have a multi-generational commitment, together with the Peninsula Trust, to preserve a gigantic swath of the square mileage of San Mateo County for non future development. But that doesn’t mean that there’s not space left to develop. There are many plots along Interstate 101, for example, where high density residential housing can be inserted inside San Mateo County. But there needs to be a broader conversation to allay the NIMBY fears of the broader population about what the impact is, in terms of foot traffic, in terms of generalized motorized traffic, if new housing is built, and I think that that conversation can unlock let’s call it social innovation in order to get these projects approved.

How Nonprofits Fund Affordable Housing Projects

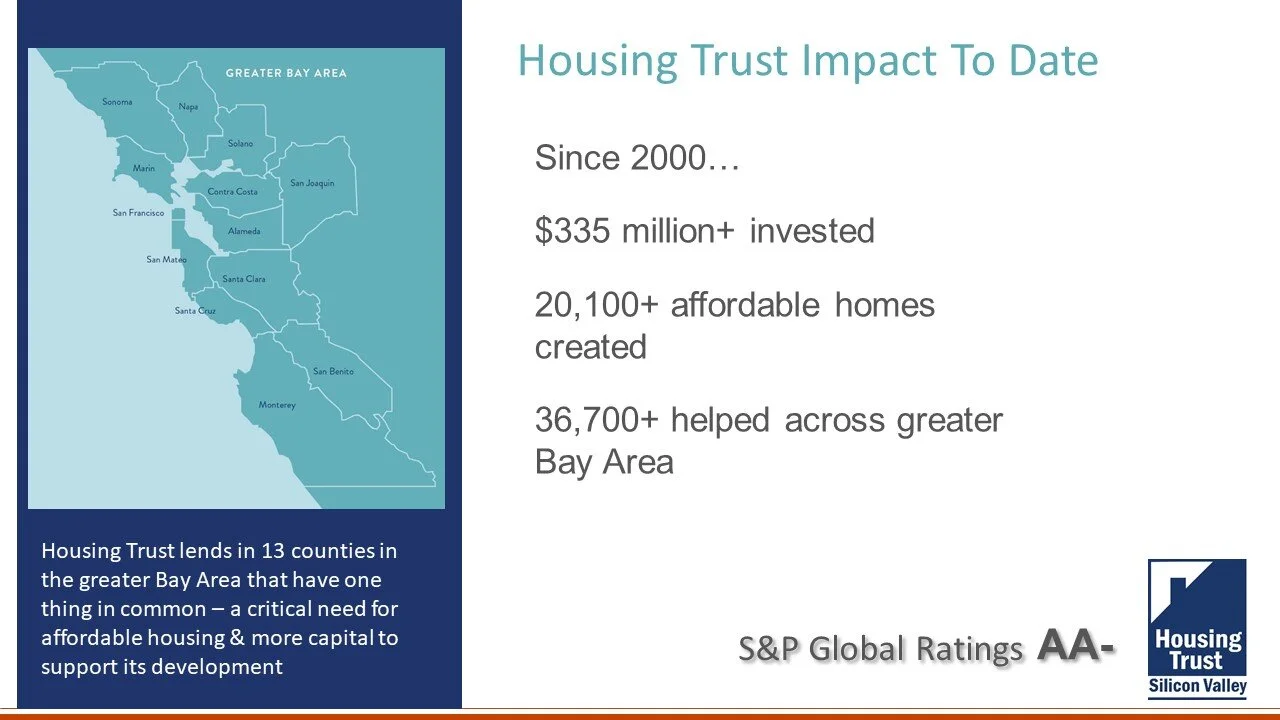

JULIE MAHOWALD, INTERIM CEO, HOUSING TRUST SILICON VALLEY Housing Trust Silicon Valley is what’s called a CDFIs, a community development finance institution. You can also think of that as a bank to the underserved. We will finance things that banks traditionally do not want to finance. There are 2,000 CDFIs in the country and their assets comprise over $200 billion. We are one of a handful of those 2,000 that have an S&P credit rating that has been renewed at double A minus. That helps us to raise funds from corporations. Our work spans homeownership programs, grants to those experiencing homelessness and even a nascent ADU loan program that we’re hoping to be able to launch later this summer.

Multifamily lending is our sweet spot. To build an affordable apartment from the ground up, or to preserve affordable housing, there’s a complex web of financing to take a developer from buying the land on the open market and then getting all the way to the long-term financing so that they could break even. Those costs don’t really change for affordable housing, so there needs to be really affordable or cheap financing available and sometimes free land. There are a lot of different subsidies that are pulled together so that when the developer finishes, they can charge below market rents. So Housing Trust is a lender in two places in this process. Traditionally, we lend to help these affordable housing developers and often they’re competing with market rate developers to purchase land or do pre-development work—getting architects ready and entitlements and all of that. We’ll lend that money in that early stage when banks do not want to lend, but then we’re traditionally taken out by a construction lender, because banks are happy to lend at that spot. The long-term piece could have all kinds of subsidies from cities, counties. There could be land donated. All of those things a developer has to pull together. They might apply to five or ten programs, but that can also often leave them in a spot where they’ve got five out of the six they applied for, but they could have a gap of $5 million in order to get shovels in the ground and start building housing.

As a CDFI, we sometimes receive grants from the federal government, we still get a little bit from states, counties, cities, as well as low cost loans from banks. Three years ago, we created something we call the community impact note for accredited investors. It’s a private placement of debt, below market rate and a social impact investment. We borrow money using the full faith and credit of our balance sheet and then we on lend that to developers. We’re very proud that we’ve raised to date $117 million in this fund, called The Tech Fund, and so far helped start up 3,000 homes in the past three years. We envisioned that private investors would buy this. What really happened is we had a lot of corporations and some philanthropists that got very excited about it. We got very large investments from Cisco, Google, LinkedIn. NetApp and Pure Storage. Sobrato, Packard and Grove Foundations also invested in this note. But recently even more of a breakthrough for these impact funds and for CDFIs around the country has been that corporations are starting to invest in really interesting ways and in not only affordable housing, but small business lending. When Google announced their social responsibility bond, a $10 billion bond offering taking advantage of really cheap rates, half of it will be used in their climate objectives, but they made a point of saying that the work they do with Housing Trust, and with other CDFIs in the country, is going to be supported by this bond also. It’s capacity building for us and we are the servicer and the advisor as they place monies in the affordable housing ecosystem.

How Nonprofits are Partnering with Developers to Create Innovative Solutions to the Crisis

COMFORT HARR In the old days, we were pretty much dependent on government for financing and financing tools for affordable housing, through community development block grants and through other pass-through funds from HUD. Really the only way we got it done was within government partnership. But over the years, that has changed quite a bit. We could sometimes have a stack of five to fifteen different funders and getting escrow to close with all those different funders at the same time was super, super hard. So as funding from government has been reduced as we lost our redevelopment agencies, we’ve had to go get really creative on how we finance and what our stack looks like. As a side note, trying to simplify those stacks is really important because the property management side on the other end. Once you have a property and you’ve got it all going, you’re accountable to every lender who’s given you money. There’s a reporting requirement that makes all of that very difficult. So just recently we closed on a project that was a first in San Mateo County. Cities now require things called impact fees and those impact fees go into funds that the cities hold so the county can use toward affordable housing. But accessing those funds can be really hard because once the impact fee is paid, say by a commercial developer or residential developer, in order to get their entitlements, the city has to figure out how then to distribute those. And that can be a very arduous process, right? It’s expensive, they have to have staff, they have to take it out for competitive bid, you have to find land. There are all these barriers to accessing the money. So as part of an acquisition strategy, we were approached by a commercial developer, Greystar, who didn’t want to pay the city the impact fee. Instead, they wanted to put it directly into affordable housing. So as part of their entitlement process to get their building permit, we went alongside them side-by-side to say we have an alternative housing plan. That is to take the equivalent of the impact fee, which in this case was $2,149,000, and put it directly into an escrow account rather than sending it to the city. As long as a property could be acquired within a certain amount of time, that money could be used to acquire the property deed restricted as affordable and preserve an existing property. The city loved the idea. It with met all that criteria met all of my criteria as a preservation specialist. But we just weren’t going to get that impact fee fast enough, so we had a social investor, a private person who came in and said, “You know what, I’m going to buy that property for you. I’m going to hold it for you. I’m going to give you the property management lease on it and you master lease it. You take care of it, as long as I don’t have to deal with it, then you can go forward and get those entitlements and get that impact fee.” What ended up happening is the purchase price was $3.3 million. The social investor was able to acquire that property for 3.1 million. We went into a purchase agreement for the original 3.3 asking price. There is revenue to be made on the social investor’s side. We felt that $3.3 million was actually a very good price for that property and that he was able to get it for $3.1 million was good for him. The owner sold it to us for $3.3 million, the developer was super happy because his money got used right away and not get stuck in a fund that was held by city. The city’s really happy because they don’t have to figure out how to use that money and the property became deed restricted and affordable immediately upon closing escrow. We’re super happy because now we have ten more units in our portfolio that didn’t exist before. Everybody wins. It’s a brand new model and we were the first to divert an impact fee directly into an acquisition. We’ve already been contacted by other cities who are interested in doing that kind of work. So if you’re looking at doing projects, talk to your city to find out how flexible they can be on some of those impact fees. It’s really an important part of the tool.

Transcribed by https://otter.ai

Talk to the financial experts at Fairlight Advisors to learn more about managing your nonprofit’s investments. Schedule a free consultation today!

Fairlight Advisors

Latest posts by Fairlight Advisors (see all)

- Market & Economic Snapshot Q1 2026 - April 29, 2026