We recently spoke to Bill Kan, the founder of Candent Capital, a firm based in the Bay Area providing financial planning, investment and wealth management services, to ask him what he thinks about all of the buzz around whether we are going to suffer another recession, after having experienced one two years ago. So Bill are we going to have a recession or not and what should nonprofit endowment investors be prepared for?

Bill Kan, Candent Capital: It’s a really interesting question. And I guess it’s top of mind for everyone, including myself. As you said, I started out as an economist and my first job out of college was working at the Fed in Washington. So thinking about this stuff is second nature to me because after going to business school, my first job was actually to be an economist on Wall Street. I was a so-called Fed watcher. Back then there were a slew of economists out there trying to read the tea leaves, trying to interpret what the Fed was doing. So right now, the Fed does tell you what it’s doing. It is saying it’s recognized that we have a huge problem. Now, inflation is at a hand. A year ago, when inflation started to tick up, I thought this could be temporary, right? We have this boat that stuck into Suez Canal–a bottleneck that should eventually clear itself. And we had excess capacity at that time, because we were still dealing at the early stages of COVID. But we didn’t know how any of this stuff was going to last. And the longer bottlenecks persist, the uglier the problems would be. So here we are now two years forward roughly, and the problems have persisted. Then we have most recently, the attack in Russia and that certainly influenced the energy markets in terms of oil and natural gas to Europe. The world is connected. As we learned last year with the Suez Canal, that all the stuff that we buy is kind of dependent on other countries. We’re not self-contained and when there are disruptions, things don’t get delivered. The longer things drag out, the more problems are created, and with that, if goods don’t get produced or delivered, we have a shortage. Remember, econ 101? Everything’s about supply and demand. If demand is the same and supply drops, prices go up. And if demand increases and supply doesn’t change, prices go up. The problem now is that demand is up and supply is down so we have inflation spiking. And the Fed is saying, “Yes, we have to address this now.” It’s actually by law, they have to do it. What I’m trying to highlight is the difficulties and the challenge of the problems. One reason why the Fed didn’t act earlier in trying to so-call, “tap the brakes” a little bit to slow down the economy is because the Fed knows it has a certain problem. We were dealing with COVID, at least at first. And this is new territory we’ve never been before, at least not for at least 100 years since the Spanish Flu. That’s one issue. The other issue is that the Fed knows from history, that it’s not very good at getting things started again. It’s good at slowing things down. In fact, the Fed knows very well that you can shut the economy down and therefore kill inflation, if you will, by raising interest rates. We saw that in the late 70s and early 80s with Paul Volcker, the former Fed Chairman, when he jacked up interest rates when inflation was in the double digits. He changed the way the Fed operated, raising interest rates and helped set off this 35-, 40-year decline in inflation and interest rates, which has been huge for many people in many different ways. But at that time, Paul Volcker also got bricks sent to him at the Fed, because people were upset, especially on homebuilding.

Maya Tussing, Fairlight Advisors: So you’ve demonstrated that this is a complex question that economists can’t easily say, “Yes, we’re poised for a recession.” And often we read that you don’t know we were in recession. It’s kind of a backward looking indicator. Can you talk about that?

Bill Kan: There’s actually a committee out there that determines recessions and growth periods. And usually, it’s after the fact a lot of times. We don’t even know we’re out of a recession until a few years later. Sometimes it’s not clear we’re in a recession until a year later. Sometimes they’re obvious, say April of 2020 when COVID really struck. But in many cases, it’s not so obvious.

Maya Tussing: Is it because it’s lagging data that determines a recession?

Bill Kan: Yes, the economic data is lagging. Some is lagging by month, some a quarter, some by longer periods. Meanwhile, people like us, we feel the pain today. The stock market can be dropping. We see that we’re writing bigger checks to pay for things. We feel that energy prices go up, and we’re thinking, “I can’t drive my car anymore.” But a lot of these things are what economists would call “transitory”, meaning it’s not permanent. The Fed Chair, for example, can’t decide to act if it’s a temporary blip. You can do a lot more damage by reacting that way. They have to think forward and methodically in order to act.

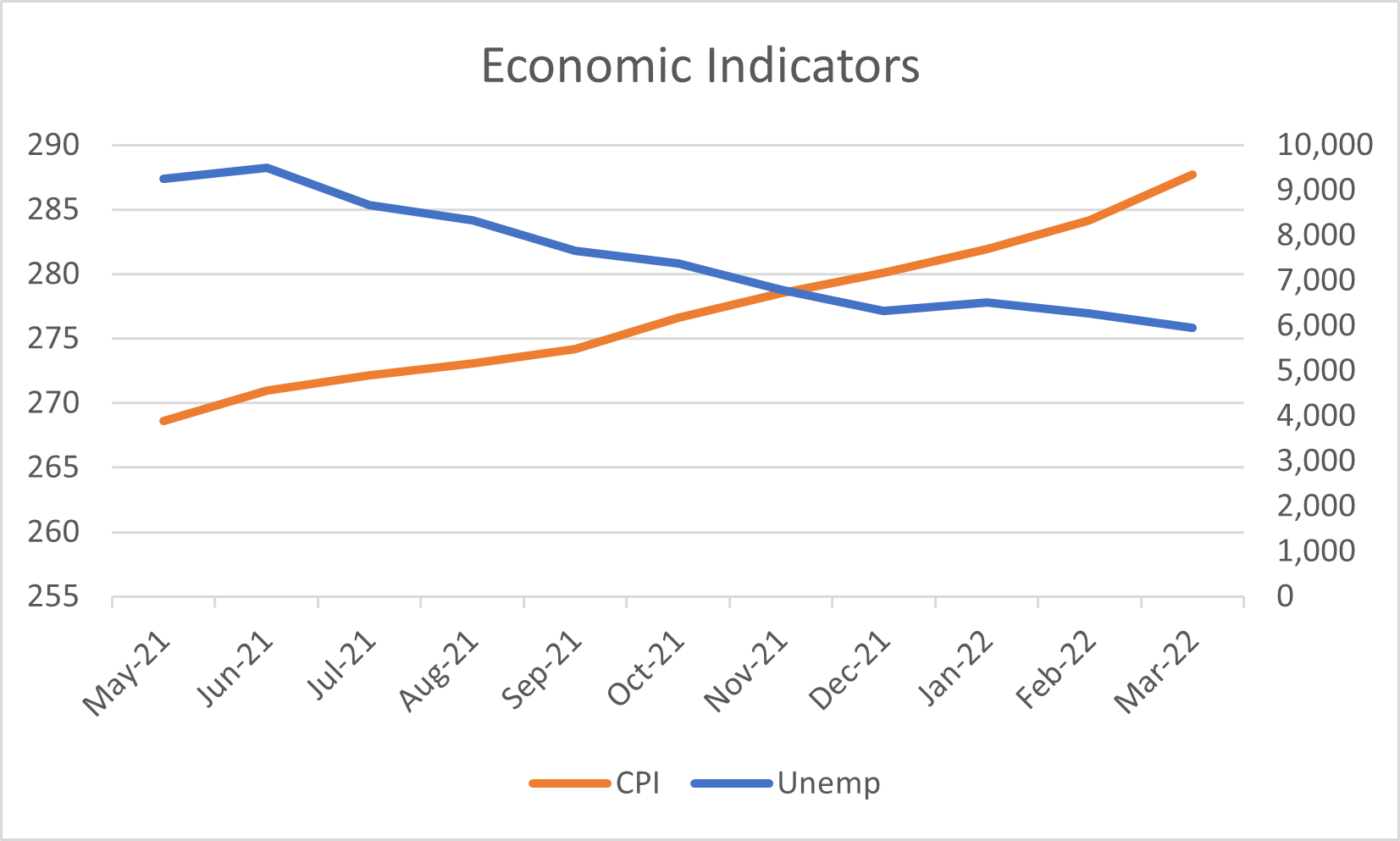

Source: Koyfin

The Central Bank needs to have have a certain gravitas for people to believe it. It has to have a strong track record. It can’t act willy-nilly. Otherwise, you can’t really trust it. If it’s under the President of the US and they nudge the Fed to say, “Oh, things are not looking good now. Make interest rates lower, so I can do better in the polls.” That doesn’t work well, in the long run. Now, the evidence is clear. Not only has inflation ticked up, it’s trended up. The current situation is that inflation has accelerated. Not only has it ticked up or trended higher, it’s rising at a faster pace.

Maya Tussing: So to close this out, what what are some of the indicators that you’re seeing that are more positive? That we might see better days?

Bill Kan: Well, if you’re looking for a job, then this is the best time ever, according to the Fed Chairman Powell. For every person looking for a job, there are 1.7 job openings. I don’t think you can argue against that. Now, granted, we’re in the Bay Area and usually, we know that there has been a shortage of people doing computer science and engineering. But that was not the case in all parts of the US. But now, it’s almost like for all types of jobs. There’s a shortage of workers. I was also looking at business formations which is about 400,000 a month.

So yes, as I look around San Francisco, there are still for lease signs, but things are happening. And we know that it’s hard for restaurants to find workers to serve or serve or cook. And that’s true for a lot of industries. I know people in biotech are having a hard time finding scientists, for example. My nephew is three years out of school and he said, “I’m gonna see if I can expand my horizons and experience something else in tech.” Within a month, he had four offers. I mentioned that because risk is a key part of it. The willingness to take risk is good for growth. And right now, there’s a lot of people starting businesses. There are still people looking to buy homes. Yes, interest rates are higher and even before the Fed start doing too much. But the environment is so good. And typically, even when the Fed starts raising interest rates, the economy doesn’t slow down immediately. It has momentum and you’d have to reverse the momentum to get things to really slow down. But what I advise a lot of folks is to prepare for a recession. Make sure you save enough. Make sure you know what’s in your back pocket. And that will help you buffer any possible bad news.

Maya Tussing: It’s the same on the institutional or nonprofit level. These “black swan” events are happening more frequently, so they may not necessarily be black swans anymore. But what I hear from you is there’s still a lot of hope, from consumers, investors, employees, and prospective employees are still seem hopeful. And so if there is a dip, at least it that it may be a soft landing.

Talk to the financial experts at Fairlight Advisors to learn more about managing your nonprofit’s investments. Schedule a free consultation today!

Fairlight Advisors

Latest posts by Fairlight Advisors (see all)

- Market & Economic Snapshot Q1 2026 - April 29, 2026