A Development Officer called us with a strange request. Could I please help a nonprofit Executive Director decide what to do with a six-figure donation? It’s not often nonprofit leaders don’t know what to do with a large gift. But this gift had a unique restriction. The money must be allocated to an account reserved for emergencies or unplanned incidents, whatever they may be; an unrestricted, restricted gift you could say.

A Development Officer called us with a strange request. Could I please help a nonprofit Executive Director decide what to do with a six-figure donation? It’s not often nonprofit leaders don’t know what to do with a large gift. But this gift had a unique restriction. The money must be allocated to an account reserved for emergencies or unplanned incidents, whatever they may be; an unrestricted, restricted gift you could say.

In 2020, nonprofit organizations had to maintain operations during a healthcare crisis, an economic recession and environmental disasters simultaneously. If at any other time, it has shown nonprofit leaders and boards the importance of strong financial resilience policies to ensure that the organization can meet expected and unexpected cash obligations at a reasonable cost.

Nonprofits operate on very thin margins, which is to say that most of the money that comes in as revenue goes right out as expenses. As a result, there’s very little wiggle room for a nonprofit to pivot quickly after an unplanned incident like an external event or even a major error. That is why cash gifts that are formally structured as an Operating Reserve provide a true lifeline for nonprofits, allowing them to be financially resilient in the face of adversity.

To be clear, this is not just a large unrestricted gift. It is a gift that should be governed by an Operating Reserve Policy, ratified by the board so it has its maximum effect.

Operating Reserve Policy in Detail

Purpose

The purpose of the Operating Reserve Policy is to ensure the stability of the mission, programs, employment, and ongoing operations of the organization. The Operating Reserve provides an internal source of funds for situations such as

- a sudden increase in expenses,

- a onetime, unbudgeted expense,

- an unanticipated loss in funding or

- an uninsured loss.

An Operating Reserve Policy may also be used for one-time, nonrecurring expenses that will build long-term capacity, such as staff development, research and development, or investment in infrastructure.

An Operating Reserve Policy would NOT allow funds to replace a permanent loss of funds or eliminate an ongoing budget gap. Additionally, the policy would stipulate that any funds used would be replenished within a reasonably short period of time.

In addition to stipulating the appropriate uses of reserve funds, the Operating Reserve Policy specifies the approval process to use operating reserves. In other words, how the Executive Director can gain approval from the Finance Committee or full Board of Directors to use the reserves.

Definitions and Goals

The Operating Reserve Policy defines the operating reserve as a designated fund set aside by action of the Board of Directors. The minimum amount to be designated as operating reserves will be established in an amount sufficient to maintain ongoing operations and programs for a set period and is typically measured in months of operating costs.

The most effective way to arrive at a nonprofit’s average monthly operating costs is to add up the last 12 months of actual cash expenses such as salaries and benefits, occupancy, office, travel, program, and ongoing professional services and then divide that sum by 12.

(12 months of actual cash operating costs) ÷ 12

= average operating monthly costs

Depreciation, in-kind, and other non-cash expenses are not included in the calculation.

But how many months in operating costs should a nonprofit maintain to fund the Operating Reserve? It depends.

In theory, the amount required to fund an operating reserve is essentially the average amount it would cost to resolve likely trouble in one year, bringing the organization back to fully operational. While there is no exact science to determine the amount of emergency reserves a nonprofit requires to stay resilient, there are a couple ways to come up with a pretty good ball-park figure.

Basic Operating Reserving Calculation

A new nonprofit or one just initiating a culture of financial resilience should build toward at least three months of operating costs as a bare minimum. In a strong economy, three months will protect against the most likely unexpected events – fundraising shortfalls, emergency repairs, technology failures or unplanned program needs. Again, this approach is the most basic in that it doesn’t involve an estimate into how off nonprofit budgets will be and by how much. If the organization budgets have a history of being somewhat accurate, then three months might be sufficient. However, if actual expenditures are often more than anticipated, more months of operating costs should be reserved.

Risk-based Operating Reserve Estimate

For organizations with budgets of around $5m or more or those aspiring to embrace a robust culture of resilience, determining the amount in operating reserve funds involves determining the nonprofit’s risk profile. Risk profile is just a fancy term to describe the organization’s ability and willingness to take chances and how much it has to lose should things go wrong in delivering on the mission.

We often recommend nonprofits look at five resilience factors to determine a nonprofit’s risk profile.

Funding – the various sources of financial support that organizations rely on to carry out their missions and sustain their operations. This includes donations, grants, sponsorships, events, sales of goods and services as well as other assets the organization relies on to support the nonprofit.

People – the individuals and groups, each playing a crucial role in the organization’s success. These include the executive team such as the Executive Director and their deputies, the board of directors, staff members and volunteers.

Programs – range of activities and processes designed to deliver services and achieve the organization’s mission. This could include resource allocation, service delivery, partner management, budgeting and scaling.

Facilities – maintaining the built environment, ensuring that it supports the organization’s goals and provides a safe, efficient, and pleasant space for everyone.

Technology – involves the strategic use of technology to enhance the efficiency and effectiveness of a nonprofit organization. This can include IT support, updates and upgrades, data management, cybersecurity, compliance, training and adaptation.

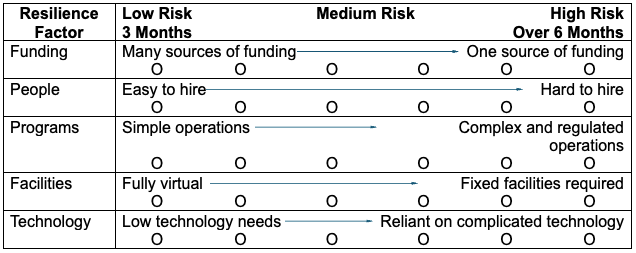

Every organization is unique in how these areas factor into a nonprofit’s resilience. In other words, a nonprofit’s risk profile is dependent on how the five areas influence its success or failure. Let’s look at each area on a spectrum from low risk to high risk.

| Resilient Factor | Low Risk | High Risk |

| Funding | Many sources of funding | One source of funding |

| People | Easy to hire | Hard to hire |

| Programs | Simple operations | Complex and regulated operations |

| Facilities | Fully virtual | Fixed facilities required |

| Technology | Low technology needs | Reliant on complicated technology |

Resilience factors on the riskier end of the spectrum are more costly to maintain, manage and resolve should things go wrong. Therefore, when a nonprofit is exposed to resilience factors on the riskier end of the spectrum, it should hold more months of expenses in operating reserves.

The guide below combines the resilience risk factors and months of reserves so a nonprofit can make a risk-based estimate for operating reserves.

To use this guide, a nonprofit would facilitate a discussion with its leadership, preferably including the board, to determine where the organization lands—low risk, high risk or somewhere in between—for each of the resilience factors.

To demonstrate, let’s assess a food bank in a large urban area to understand how they might assess the organization’s risk profile to determine operating reserves.

Funding Resilience: Food banks are at risk of being overly reliant on a few funding sources. Also, food banks tend to be doubly squeezed during times of economic instability which leads to both reduced donations and increased community need. Let’s assess this as medium risk tending toward high.

People Resilience: High reliance on volunteers can be risky if there’s a sudden drop in volunteer availability. Frequent changes in staff can disrupt operations and lead to a loss of institutional knowledge. Let’s assess this factor at medium risk as well but tending toward low.

Program Resilience: Ensuring all programs comply with local, state, and federal regulations is crucial to avoid legal issues. Program operations are complex and require adequate training to avoid mishandling of food or safety incidents.

Facilities Resilience: Poorly maintained facilities can lead to health and safety hazards. Limited storage and distribution capacity can hinder the ability to meet demand. The location of facilities can impact accessibility for both volunteers and beneficiaries.

Technology Resilience: Dependence on technology for operations means that system failures can disrupt services. As with any organization, there is a risk of cyber-attacks that could compromise sensitive data.

Based on the results of this example assessment, it might be prudent for a food bank to hold up to five months of operating reserves to ensure that the mission is sustained through challenging times. That means an urban food bank with a budget of $10 million would need to always maintain approximately $4 million liquid reserves. This can be a substantial number to maintain continuously, especially for organizations that struggle to raise funds. However, allocating enough cash toward the nonprofit’s operating reserve – whatever amount leadership determines is appropriate –should be a priority to safeguard the organization’s resilience. Once leadership establishes the amount required to fund the operating reserves, they can finalize the Operating Reserve Policy with plans on how to fund reserves and which expenses are approved.

Funding of Reserves

Nonprofits typically fund operating reserves with surplus unrestricted operating funds. The Board of Directors may from time to time direct that a specific source of revenue be set aside for Operating Reserves. Examples may include one-time gifts or bequests, special grants, or special appeals. Again, this can be difficult for nonprofits that struggle with funding, but an organization that is laser focused on surpluses to fund an operating reserve above all will be more resilient for it.

Permissible Investments

Operating reserves should invest in assets that prioritize liquidity and capital preservation, ensuring that the investment can be converted to cash without the value of the investment losing value. For more information on matching nonprofit funds to the appropriate investment strategy, refer to Investing Nonprofit Funds. An Operating Reserves policy should stipulate permissible investments that are liquid and preserve capital, such as:

- FDIC Insured Savings Accounts

- FDIC Insured Money Market Accounts

- FDIC Insured Certificates of Deposit

- Overnight Investment Grade Commercial Paper

- Securities issued or guaranteed by the U.S. Treasury

- Securities issued or guaranteed by any other U.S. government agency

- Municipal bonds with demonstrated liquidity

- Publicly traded mutual funds or ETFs composed entirely of permissible investments

Use of Reserves

Finally, an Operating Reserve Policy should determine the process to use funds. First, keep reserve funds separate from operating funds to avoid unintentional use. Your organization can manage this through separate accounts at your nonprofit’s financial institution. When it comes to spending reserves funds, most policies stipulate that the nonprofit Executive Director and staff identify the need for reserve funds and confirm that the use is consistent with the purpose described in the Policy. This step requires analysis of the reason for the shortfall, the availability of any other sources of funds before using reserves, and evaluation of the time period that the funds will be required and replenished. Upon approval for the use of operating reserve funds, the Executive Director will maintain records of the use of funds and plan for replenishment.

Putting it All Together: Reporting

Resilient nonprofits include their reserve levels in regular financial reports to the board and stakeholders. This ensures the organization is following the guidelines within the Operating Reserve Policy. Regular review of operating reserves also allows nonprofit leadership to adjust reserve policies and levels based on changes in the organization’s financial situation and strategic goals. For example, a nonprofit can report quarterly reserve balances versus average quarterly expenditures to ensure the operating reserve policy amount is tracking with changes in nonprofit financials.

By maintaining and tracking operating reserves, nonprofits can better navigate financial challenges and ensure long-term sustainability.

Operating reserves are one of the most essential elements of a nonprofit resilience program, ensuring the stability of the mission, programs, employment, and ongoing operations of the organization. Nonprofits that formalize the maintenance and use of operating reserves with an Operating Reserve Policy are among the most robust in the sector.

In the next chapter, we will explore how a nonprofit can spend endowment funds.

Fairlight Advisors

Latest posts by Fairlight Advisors (see all)

- Market & Economic Snapshot Q1 2026 - April 29, 2026